FBT refers to Fringe Benefits Tax and even though it is not directly related to the payroll, reportable values will need to appear on the employee’s ATO payment summary.

If an employee has a Reportable Fringe Benefit Value, commonly known as Grossed-up Taxable Value in excess of $2000.00, the Grossed-up Taxable Value must appear in STP reporting and so optional ATO payment summary production. These amounts are calculated from 1 April – 31 March.

The Reportable Fringe Benefits Amount is the Grossed-up Taxable Value of certain fringe benefits provided to you by your payer for the FBT year (1 April to 31 March), where the taxable value of those benefits exceeds $2,000.

Click here to read more on ATO's website.

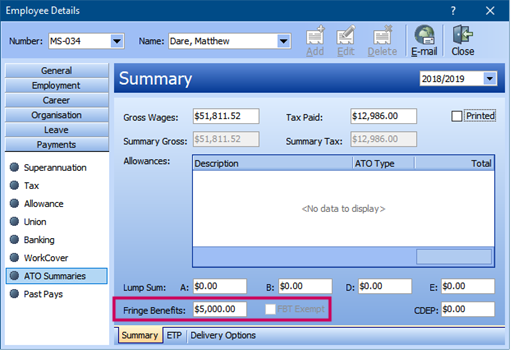

The Grossed-up Taxable Value is entered directly into the ATO Payment Summaries screen under the Employee > Edit Employee > Payments > ATO Summaries > Fringe Benefits.

In the 2016/2017 financial year, Fringe Benefit reporting changed to accommodate Exempt Fringe Benefit.

Types of organisations that are exempt from paying FBT include public benevolent institutions, health promotion charities, public and not-for-profit hospitals and public ambulance services.

Please check with your accountant or seek advice from the ATO with regards Non- Exempt and Exempt Reportable Fringe Benefits.

Comments