From the financial year ending 2016/17, the ATO has made changes to the reporting requirements for company’s and employees who receive fringe benefits.

- Types of organisations that are FBT exempt, that is, exempt from paying FBT, include public benevolent institutions, health promotion charities, public and not-for-profit hospitals and public ambulance services.

- Further information on these types of organisations and capping thresholds available on the ATO website.

- There is an option in File> Company Details >Taxation >Tax Configuration to allow for setting the company as FBT Exempt.

- When selecting this option, the employee is automatically set to FBT Exempt also within the employee file under Employees > Payments > ATO Summaries.

- Please continue to enter any reportable Fringe Benefits amounts in the relevant field in the employee file.

Please Note

If an employer provides multiple fringe benefit amounts to the same payee in the same fringe benefit period and at least one amount complies with section 57A of the Fringe Benefits Tax Assessment Act 1986 and at least one other amount does not comply, then two separate payment summaries are required.

Further information on reportable fringe benefits available on the ATO website.

In the instance that an organisation has an employee who has worked two roles, where one is FBT exempt and the other role not, a second employee file will need to be created to accommodate the non-exempt role (untick the FBT Exempt box within the employee file) and required second ATO Payment Summary. This second employee file would contain no payslip data, simply the manually entered reportable fringe benefit value and unticked FBT Exempt setting.

STP

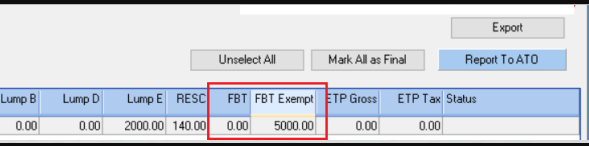

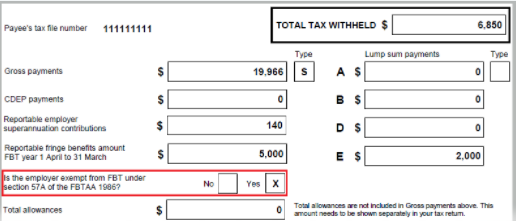

Depending on whether or not the FBT Exempt box is ticked or not, the employee FBT will either appear in the Exempt box (Example above) or FBT box in STP (ATO Payment Summary which is no longer required, will either be marked as No or Yes against Is the employer exempt from FBT under section 57A of the FBTAA 1986?).

Please Note

If there is no reportable fringe benefits amount entered in Employee File under Payments > ATO Summaries – Fringe Benefits and regardless of the FBT Exempt indicator, then the No and Yes boxes for the Is the employer exempt from FBT under section 57A of the FBYAA 1986? on the ATO Payment Summary will be left blank.

Comments